Bank Reconciliation General Journal Entries

Work With Basic Journal Entries

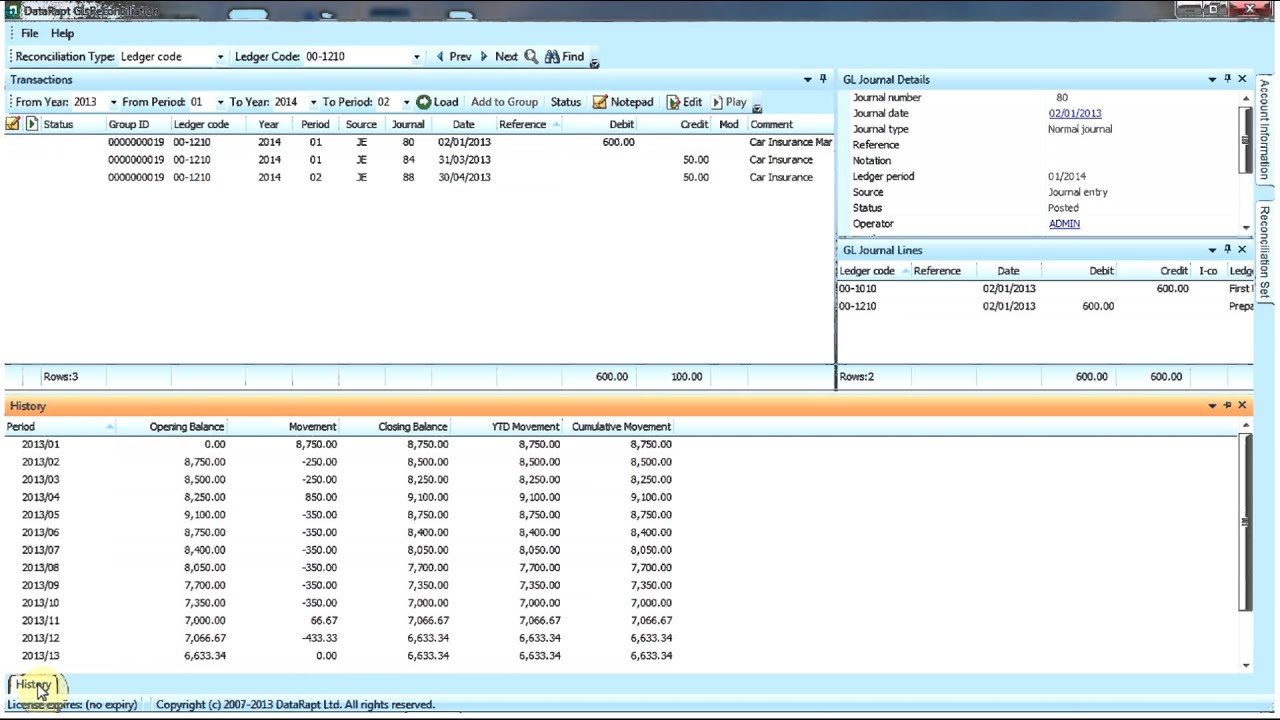

General Ledger Reconciliation Youtube

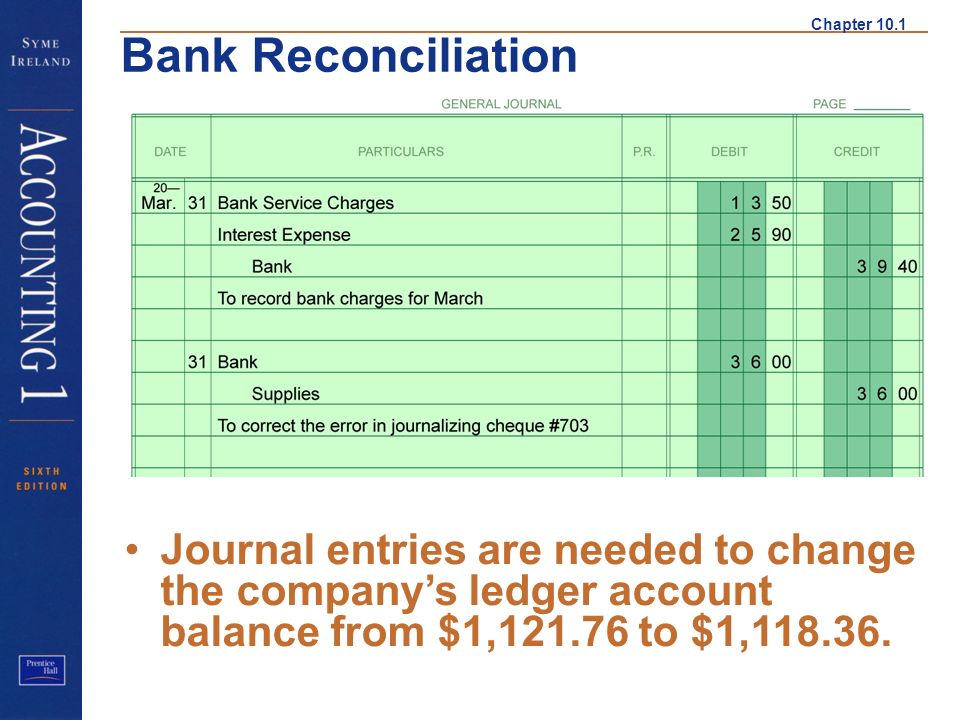

Chapter 10 1 Bank Reconciliation Heading Write The Heading Ppt

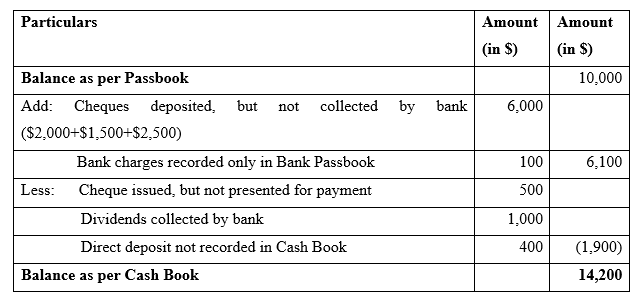

Bank Reconciliation Example Best 4 Example Of Bank Reconciliation

Psa L P Bank Reconciliation How Voiding A Pseudo Check Affects

Bank Reconciliation

Make A Journal Entry General Journals Procare Support

What journal entries are prepared in a bank reconciliation.

![]()

Bank reconciliation general journal entries. Reconciling a journal entry on bank reconciliation. The bank statement for august 2019 shows an ending balance of 3490. Click here to see the original bank reconciliation video. On august 31 the bank statement shows charges of 35 for the service charge for maintaining the checking.

I have written a few general journals to correct entries on my bank account in my general ledger. Journal entries hit the cash account on the ledger. Riaan louw over 10 years ago. The accounting concepts of.

Definition of journal entries in a bank reconciliation. For example to record a bank fee in an account holders books debit the bank fee account and credit the cash account. Im simply trying to get this client caught up but how can i do that when i cant reconcile the bank. These entries serve to record the transactions and events which impact cash but have not been previously journalized eg nsf checks bank service charges interest income.

Clear this check box to post all deposit transactions for an entry as separate entries in the bank reconciliation module. Examples of journal entr. This check box is available only if the bank reconciliation module is integrated with general ledger and deposit is selected at the transaction type field in the transaction journal format window. Learn how to journalize the entries required at the end of a bank reconciliation.

Sample bank reconciliation with amounts. In this part we will provide you with a sample bank reconciliation including the required journal entries. Journal entries for bank reconciliation the items on the bank reconciliation that require a journal entry are the items noted as adjustments to books. In each case the bank reconciliation journal entries show the debit and credit account together with a brief narrative.

The majority of transactions are jes and reconciling the bank. They do so by debiting and crediting financial accounts such as assets liabilities and expenses. These are the items that appear on the bank statement but are not yet recorded in the companys general ledger accounts. We will assume that a company has the following items.

They are reflected as cleared in the bank reconciliation even though it will not let me see those to check them or not. Once the correct adjusted cash balance is satisfactorily calculated journal entries must be prepared for all items identified in the reconciliation of the ending balance per company records to the correct cash balance. Journal entries are required in a bank reconciliation when there are adjustments to the balance per booksthese adjustments result from items appearing on the bank statement that have not been recorded in the companys general ledger accounts. The bank reconciliation journal entries below act as a quick reference and set out the most commonly encountered situations when dealing with the double entry posting relating to bank reconciliation adjustments.

I have way too many entries to go back and delete each one.